Landlord Blog

Education and news for smart DIY landlords!

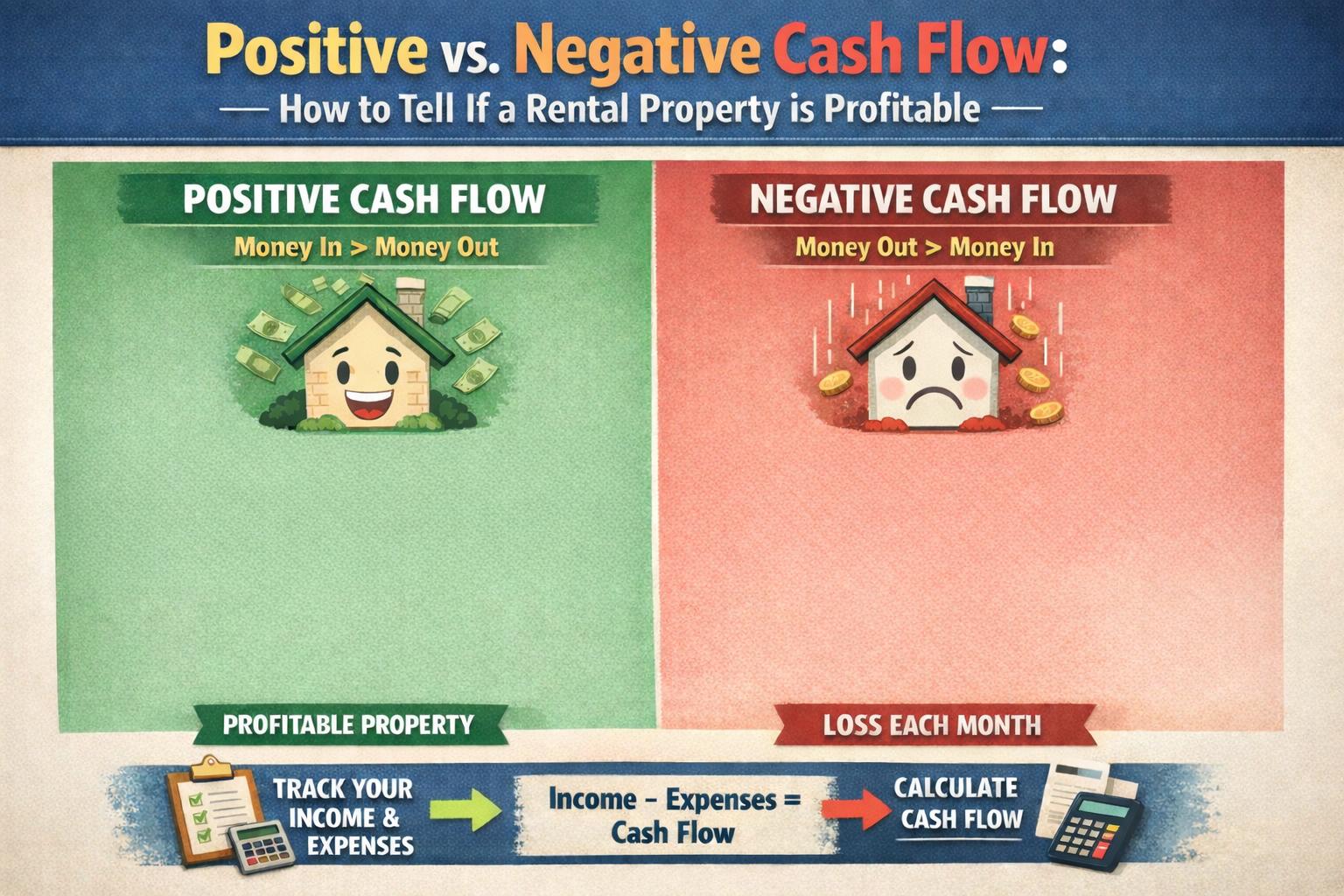

Positive vs. Negative Cash Flow: How to Tell If a Rental Property is Profitable

Cash flow is one of the most important factors in determining whether a rental property is truly a good investment. While appreciation and tax benefits matter, steady monthly income is what keeps a property sustainable over time. For both new and experienced investors, understanding the difference between positive and negative cash flow can make the difference between building wealth and taking on financial stress.

What Cash Flow Really Means

Cash flow is the money left over after all rental income is collected and all expenses are paid. To calculate it, you subtract your total monthly expenses from your total monthly rental income. Expenses include your mortgage payment, property taxes, insurance, maintenance, repairs, property management fees, and any homeowner association dues. If there is money left over at the end of the month, the property has positive cash flow. If expenses exceed income, the result is negative cash flow.

Positive Cash Flow Explained

A property with positive cash flow generates more income than it costs to operate. This means rent not only covers the mortgage but also ongoing expenses, leaving you with extra money each month. Positive cash flow provides financial breathing room and can help cover unexpected repairs or vacancies without dipping into personal savings. Over time, this surplus can be reinvested into additional properties or used to pay down debt faster.

Positive cash flow properties are often found by purchasing below market value, putting down a larger down payment, or investing in areas with strong rental demand and reasonable property prices. While these properties may not always be in trendy neighborhoods, they often offer stable, long-term returns.

Discover: What to Look for When Evaluating Rental Properties

Negative Cash Flow Explained

Negative cash flow occurs when rental income does not fully cover expenses. This means you are paying out of pocket each month to keep the property afloat. Some investors accept negative cash flow in hopes of future appreciation or rent increases. While this strategy can work in certain high-growth markets, it carries more risk, especially for first-time investors.

Negative cash flow can become stressful if the property experiences vacancies, major repairs, or changes in interest rates. Without a strong financial cushion, ongoing losses can quickly outweigh potential long-term gains.

How to Tell If a Rental Property Is Profitable

To determine profitability, start with realistic rent estimates based on comparable properties in the area, not best-case scenarios. Next, list all expenses, including a maintenance reserve and vacancy allowance. Many investors underestimate these costs, which leads to overly optimistic projections.

A simple rule of thumb is the cash flow formula: monthly rent minus monthly expenses equals cash flow. A positive number suggests profitability, while a negative number signals caution. You can also calculate cash-on-cash return to see how much income the property generates compared to the cash you invested upfront.

Read more: Everything You Need to Know About Making a Rental Property Profitable

Final Thoughts

Positive cash flow is often the safest and most sustainable path for rental property investors, especially those just getting started. While negative cash flow investments can work under specific conditions, they require careful planning and financial resilience. By focusing on accurate numbers and realistic expectations, you can confidently evaluate whether a rental property will support your financial goals or quietly drain your resources over time.